According to Christensen et al. (2015), corporate tax avoidance means using the legal strategies to adjust the financial circumstances of an individual to lower the amount of tax the said individual is owing to the state. Corporate tax is achieved through claiming permissible credits and deductions. Most often, corporate tax avoidance is usually confused with tax evasion. Although the two phrases could sound similar, however, Armstrong et al. (2015) believe that tax evasion applies illegal techniques like under reporting the income of an individual to make him or her avoid paying the taxes. According to Sikka (2010) tax avoidance strategy of a given corporation is an ‘organized hypocrisy.’

Avoidance Strategy as an Organized Hypocrisy

I agree with Sikka’s Term that tax avoidance is an organized hypocrisy. Just to mention, companies tend to excel at speaking on social responsibilities when at the same time they devising structures to enable them evade paying taxes. The tenacity of corporate tax avoidance as well as the evasion lures a devotion to organized hypocrisy which can be properly comprehended as the gaps that exist between the decision, the action and the corporate talk, (Brunsson, 1989, 2003). Corporate tax avoidance is indeed an organized hypocrisy.

In particular, a case of WorldCom, which is a US telecommunications organization, collapsed amid of allegations of fraud in the year 2002. Consequently, the second reason why I agree with Sikka’s claim that corporate tax avoidance is an organized hypocrisy is the case of KPMG that was borrowed in 1997 considering the initial fee of three million dollars. Later, KPMG recouped a half a million dollars fee which meant to carter for the feasibility study. Notably, the organization proceeded to earn the bonuses of performance totaling to extra two million dollars.

Main Costs of Tax Avoidance

According to Koester, Shevlin, and Wangerin, tax avoidance will keep on inflicting and results to costly consequences to millions of individuals as long as the leaders of low-income countries are excluded from the tax avoidance solution (2016). Notably, in July 2014 at Los Angeles College, President Obama proclaimed loudly that those who employed creative measures to ensure their taxes were reduced were merely corporate deserters renouncing their citizenship to shield profits. Gaertner (2014) reveals that such strategies by individuals to avoid corporate tax have severe costs. There are five main cost types which are generated by companies and individuals vigorously avoid tax.

First, the authorities handling tax collection attempt to counter ingenious tax avoidance practice and institute new opinions and regulations which in turn become supplementary to the tax code. Although the purpose of this measure is to increase certainty, however, the end results is a convoluted tax which leads to the second cost of tax avoidance which is corporate compliance cost.

The third cost of corporate tax avoidance is increasing the cost of administration. Forth, tax avoidance encourages the formation of lobbyists and tax specialist industries which are created to exploit the system. The last main cost of tax avoidance is the loss of the government revenue. According to Hanlon (1994) and Sikka (2003), the federal government of the United States losses fifty to one hundred and seventy billion dollars annually due to tax avoidance.

Key Issue Surrounding Tax Avoidance

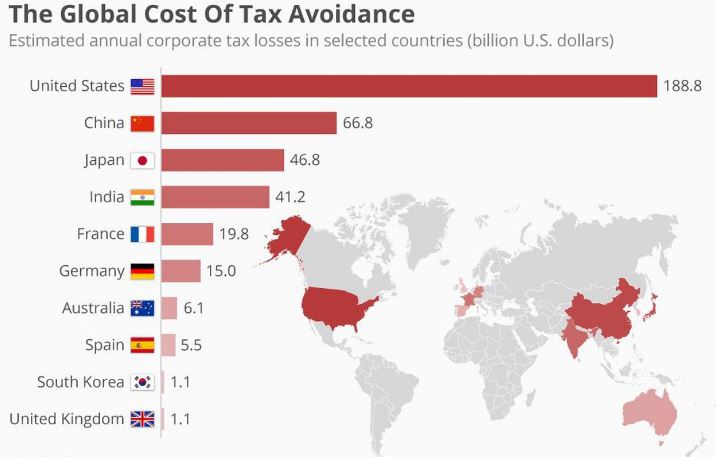

According to the Guardian on 30th March 2009, developing countries often receives approximately one hundred and twenty billion dollars from G20 countries in the foreign aid in which the said developing countries are losing an approximate amount of between eight billion and one trillion dollars from the unlawful financial outflow every year to the countries of the west (Kar & Cartwright-Smith, 2008). As Baker (2005) and Cobham (2005), about five hundred billion dollars is lost over a variety of corporate tax avoidance structures in which a substantial amount is attributed to price practices which shifts profits from the developing countries to already developed countries.

Tax is a major cost to many companies and they formulate strategies which ensure that such costs are minimized thus causing tax avoidance. According to Finch (2004), although rules still remain to be rules, nevertheless, they are prone to be broken and thus no matter which legislations are in place, the lawyers and the accountants will always find a way around the game of tax avoidance. Multinational is the leading case studies of tax avoidance since they have multiple locations which allow them to organize profits in those countries which are favorable tax regimes (Bowler, 2009).

Moral and Economic Implications of Corporate Tax Avoidance

In my own thoughts, corporate tax avoidance has negative moral and economic implications. The company which avoids tax uses the definition of CSR and also relies on a set of moral principles to assess their taxpaying behaviors using the lens of morality and ethics. However, moral reasoning is more complex than one can imagine. Following the thoughts of KMPG (2006), tax payment forms a key responsibility in the contemporary corporation. Some people usually consider paying corporate tax as a moral problem although others find it as being moral while a good portion will find the payment of corporate tax as an immorality.

On the other hand, economic implication of corporate tax is that it makes accounting companies be capitalist and thus cannot buck the system pressure to raise their own profits thus creating new tax avoidance schemes and reducing the contribution to the government (Sikka, 2005). When the tax is not collected fully, the accumulated tax compels the government to stop spending in critical areas like welfare and schools which leads to underdevelopment.

Ways in Which Corporate Tax Avoidance can be Restricted

I think that there are ways that can be used to restrict corporate tax avoidance. First is through legislation. Legislation can be achieved through standardizing corporate reporting systems to make the government process information and also compare taxes across firms to see who is avoiding the corporate tax. The legislation should aid in the detection of fraud and strictly monitor a company’s insiders on the matters of tax.

The legislation on the tax avoidance can be enforced through well-functioning courts through playing the central importance of law enforcement of the contracting parties. The other way in which tax avoidance can be restricted is through ensuring proper accounting standards. Leuz et al report that proper accounting standards bring about a global reporting coverage than often thought (2003). Single sets of accounting cannot sufficiently compare reporting and disclose any malpractice.

Harmonization of Accounting Standards- Implementation and Challenges

It is argued that there should be standardization of the accounting policy among nations to fully realize the global economy. Harmonization of accounting standards facilitates international transactions as well as minimizing the costs of exchange through the provision of standardized information to the world’s economy. The harmonization is done by the International Accounting Standards Committee (IASC), the International Accounting Standards Board (IASB) and the International Financial Reporting Standards (IFRS). The said bodies are mandated to implement the accounting standards across the world.

However, there are challenges faced during the implementation. First is the challenge of comparability. Comparability can be achieved through like things looking alike as well as unlike things looking unlike (Trueblood, 1966). According to Truebold, “things” in the accounting include the regulatory culture, the culture of auditing, the culture of account as well as the financial and business culture. The other challenge is associated with the problem of interpretation in which language is a problem when translating IFRS from English or to English.

Most accounting standards are limited in bringing convergence. It should be noted that adopting a single set of accounting cannot be sufficient to allow comparability as well as disclose relevant practice even if the said principles are compulsory to all the countries. However, the idea of adopting common sets of accounting standards cause more comparable reporting techniques as well as high-quality accounting standards like the IFRS (Leuz et al. 2003). Adopting IFRS requires that the party countries must have the asset pricing market which provides accounting values.

High accounting standards cause high quality and transparent reporting to most companies. In addition, IFRS causes economic benefits as well as cost saving. When harmonizing the accounting standards, there is a challenge of public versus private owned enterprises which includes the related party transactions. Following the observation above, the issue of comparability in accounting becomes a problem because tricky auditing problems arises (Leuz et al. 2003).

The harmonization of accounting standards requires the implementation guidance. According to Baker (2005), the IFRS have the implementation guidance to the accounting standards either through the non-authoritative guides or being standard themselves. For instance, IFRS issued the share-based guidance which is made up of forty four paragraphs relating to the application guidance. Similarly, the body issued non-authoritative guidance which guides the implementation of IFRS to guide the harmonization of the accounting standards.

The IASB body on the other hand created the international financial reporting interpretation committee which oversees the share-based payment guidance. However, Trueblood (1966) believes that the countries and enterprises which apply the IFRS in their accounting standards will become more heterogonous in terms of the size, the jurisdiction, the ownership structure as well as the structure of the capital and there will be an increase the degree of accounting sophistications.

According to Brunsson (1989), the international convergence on the harmonization of standards demands that the implementation of IFRS policies and guidance must be increased in order to achieve the intended accounting standards. The scholar adds that if the IASB committee fails to respond to the demands concerning the detailed implementation guide of the accounting standards, then the preparers of the harmonized standards must look for the implementation guidance from elsewhere.

The preparers can turn to EITF consensus to obtain answers to the questions concerning the application of IFRS. On the contrary, the form of convergence generated above is not as a result of cooperative behavior or the joint decision but as a result of auditors and preparers who seek guidance from a non-IASB credible source.

The implementation of the harmonization of the accounting standards exhibits a challenge in which the individual party countries’ financial reporting outcomes which are partly determined by the requirements of the accounting standards and partly by the incentives. The premise of the financial reporting outcome is that the accounting standards requires sufficient judgment by the preparers and auditors so that the figures reported are materially affected by the incentives of the financial reporting outcomes and the requirements of the accounting standards. Nevertheless, the typical relationship between the accounting standards and the incentives of the financial reporting outcomes is not well understood which forms part of the challenges in the implementation of accounting standards.

Leuz et al. (2003) institute that allowing the adoption of the IFRS will allow for the test of incentives that interacts with two or more standard regimes within the accounting standards. Warfield et al (1995) reveals that the financial reporting outcome is majorly affected by the ownership structure of the international accounting structure. The evidence which is available on the above claim reveals the marked specific jurisdiction differences in the ownership structure that affects the harmonization of the accounting standards.

La Porta et al. (1999) have analyzed the ultimate ownerships of the mid and large size firms in the twenty seven wealthy countries and identified four types of ultimate owners who play a key role in the accounting standards. The types include the public held non-financial institutions, the public owned financial institutions, the families and individuals as well as the state. The ownership structure of an enterprise needs to be considered before making implementations on the harmonization of the accounting standards.

Harmonization of the accounting standards requires the globalization of the trends involving the technology as well as globalization of finance. In the United States comparability of the financial data is one of the major driving forces behind the accounting standards. The comparability has been within the companies of the United States until 1980s where they began focusing on the capital markets. Some countries prefer comparability while others do not (Leuz et al. 2003).

In 1991 the FASB board was challenged to become more actively involved in globalizing trends and the internationalization of the accounting standards. The plan published by FASB instituted the objectives for achieving comparability between the accounting standards of the United States and the major national standards-setting bodies.

References

Armstrong, Christopher S., Jennifer L. Blouin, Alan D. Jagolinzer, and David F. Larcker. “Corporate governance, incentives, and tax avoidance.” Journal of Accounting and Economics 60, no. 1 (2015): 1-17.

Avoidance: Some Evidence and Issues. Accounting Forum, Vol. 29(3), 325-343.

Baker, R.W. (2005), Capitalism‘s Achilles Heel, New Jersey: John Wiley.

Beresford, D.R., Katzenbach, N. and Rogers Jr., C.B. (2003). Report Of Investigation by The Special Investigative Committee of the Board Of Directors Of WorldCom, Inc. Washington DC.

Bowler, T. (2009, February). Countering tax avoidance in the UK: Which way forward? Institute for Fiscal Studies. Discussion Paper No. 7.

Brunsson. N. (1989), ―The Organization of Hypocrisy: Talk, Decisions and Actions in Organizations‖, John Wiley, Chichester.

Christensen, D. M., Dhaliwal, D. S., Boivie, S., & Graffin, S. D. (2015). Top management conservatism and corporate risk strategies: Evidence from managers’ personal political orientation and corporate tax avoidance. Strategic Management Journal, 36(12), 1918-1938.

Christensen, J. and Murphy, R. (2004), ―The Social Responsibility of Corporate Tax Avoidance: Taking CSR to the Bottom Line‖, Development, Vol. 47 No. 3, pp. 37-44.

Cobham, A. (2005). ―Working Paper 129: Tax Evasion, Tax Avoidance, and Development Finance‖. The University of Oxford Finance and Trade Policy Research Centre.

Gaertner, F. B. (2014). CEO After‐Tax compensation incentives and corporate tax avoidance. Contemporary Accounting Research, 31(4), 1077-1102.

Hanlon, G., (1994). The Commercialisation of Accountancy: Flexible Accumulation and the Transformation of the Service Class, London: Macmillan.

Kar, D. and Cartwright-Smith, D. (2008). Illicit Financial Flows from Developing Countries: 2002—2006. Washington DC: Global Financial Integrity.

Koester, A., Shevlin, T., & Wangerin, D. (2016). The role of managerial ability in corporate tax avoidance. Management Science, 63(10), 3285-3310.

KPMG, (2005). ―KPMG International Annual Review 2005, KPMG.

La Porta, R., Lopez-de-Silanes, F., Shleifer, A. and Vishny, R. (1998) Law and finance, Journal of Political Economy, 106, pp. 1113–1155.

La Porta, R., Lopez-de-Silanes, F. and Shleifer, A. (1999) Corporate ownership around the world, Journal of Finance, 54, pp. 471–517.

Leuz, C., Nanda, D. and Wysocki, P. (2003). ‘Earnings management and investor protection: an international comparison’. Journal of Financial Economics, 69: 505– 527.

Sikka, P. and Hampton, M.P. (2005). The Role of Accountancy Firms in Tax.

Trueblood, R.M., 1966. Accounting principles: the board and its problems, in Empirical Research in Accounting: Selected Studies 1966, The Institute of Professional Accounting, Graduate School of Business, The University of Chicago, Chicago, pp. 183–191.

US Bankruptcy Court Southern District of New York, (2004). Third and Final Report of the Insolvency Examiner: In re WORLDCOM, INC., et al, Chapter 11, Case No. 02-13533 (AJG), Kirkpatrick & Lockhart LLP, Washington DC.

Werther Jr., W.B., and Chandler, D., (2005). Strategic Corporate Social Responsibility: Stakeholders in a Global Environment. London: Sage.

Relevant Blog Posts

Finance Dissertation Topics | Accounting Dissertations

Tax Fairness and Tax Efficiency