AI Adoption and Business Performance Dissertation – In recent years, the rapid advancement of technology has transformed the way businesses operate. One of the most significant technological developments is the adoption of Artificial Intelligence (AI). In the United Kingdom, the Information Technology (IT) sector stands at the forefront of embracing AI to enhance its operations and improve business performance. My dissertation project, “Assessing the Impact of AI Adoption on Business Performance in the UK IT Sector,” delves into this intriguing intersection between technology and business.

Understanding the Significance of AI in the UK IT Sector

AI refers to the simulation of human intelligence processes by machines, particularly computer systems. Its applications span various industries, including finance, healthcare, manufacturing, and of course, IT. In the UK, the IT sector plays a crucial role in driving innovation and productivity. With the advent of AI, IT firms are leveraging this technology to streamline processes, make data-driven decisions, and gain a competitive edge in the market.

The Research Methodology

To unravel the impact of AI adoption on business performance in the UK IT sector, my dissertation project employs a comprehensive research methodology. Through the collection of primary data via questionnaires, I aim to gather insights directly from professionals working in the field. A deductive approach coupled with quantitative techniques enables a systematic analysis of the data, ensuring robust findings.

Key Findings and AI Adoption Insights

Preliminary findings from the research highlight the significant influence of AI adoption on business performance within the UK IT sector. Companies that have embraced AI technologies experience improvements in efficiency, productivity, and overall competitiveness. However, challenges such as skill gaps, resource constraints, and ethical considerations emerge as barriers to widespread AI adoption.

AI Adoption and Implications for Businesses

For IT firms operating in the UK, the findings of this research project carry profound implications. Recognizing the transformative power of AI, businesses are urged to invest in employee training and development to harness the full potential of AI technologies. Moreover, the development of clear policies and frameworks that promote responsible AI usage is paramount to mitigate potential risks and ensure ethical practices.

As the landscape of AI continues to evolve, further research is warranted to delve deeper into its implications for business performance. Exploring topics such as the impact of AI on job roles, gender disparities in AI adoption, and the role of AI in driving innovation can offer valuable insights for academia and industry alike.

Conclusion

In conclusion, this dissertation project sheds light on the transformative impact of AI adoption on business performance within the UK IT sector. By examining the current landscape, identifying key challenges, and proposing actionable recommendations, this research contributes to the ongoing discourse on technology-driven innovation. As businesses navigate the digital age, embracing AI presents both opportunities and challenges. By embracing a proactive approach and leveraging AI responsibly, UK IT firms can chart a course towards sustained growth and success in an increasingly competitive global market.

If you enjoyed reading this post on Artificial IntelligenceAdoption and Business Performance, I would be very grateful if you could help spread this knowledge by emailing this post to a friend, or sharing it on Twitter or Facebook. Thank you.

In the ever-evolving landscape of business, robust marketing strategy frameworks are the linchpin that propels organisations towards success. As postgraduates delving into the intricacies of the corporate world, it becomes imperative to grasp the key aspects of marketing strategy that can make or break a brand. This comprehensive guide aims to explore the fundamental elements of marketing strategy, providing insights rooted in academic rigor and real-world applicability.

1. Understanding the Essence of Marketing Strategy Frameworks

1.1 Defining Marketing Strategy: A Holistic Approach

In the intricate tapestry of business, marketing strategy stands as the overarching framework that shapes an organization’s path to success. To truly understand the essence of marketing strategy, we must delve into its multifaceted nature and the interconnected elements that contribute to its effectiveness.

Strategic Integration Across Business Functions: Marketing strategy isn’t an isolated function; it’s an integral part of the broader business strategy. This integration ensures that marketing efforts align seamlessly with overall organizational goals. From product development to sales and customer service, every facet of a business should harmonize to deliver a unified and compelling brand experience.

Balancing Short-Term Tactics with Long-Term Vision: While tactical maneuvers are essential for immediate gains, the essence of marketing strategy lies in its ability to balance short-term objectives with a long-term vision. It’s about cultivating sustained growth and resilience against market fluctuations. This requires a delicate interplay of agility and foresight, allowing organizations to navigate the present while positioning themselves strategically for the future.

1.2 The Evolution of Marketing Strategy: Navigating Change

Historical Perspectives: Understanding the essence of marketing strategy framework necessitates a journey through its historical evolution. Traditional marketing was often synonymous with outbound techniques, where businesses broadcasted their messages to a broad audience. Over time, this paradigm shifted towards more targeted and customer-centric approaches.

Adaptations in the Digital Era: In the contemporary landscape, the digital revolution has ushered in a new era of marketing. The advent of social media, data analytics, and e-commerce has transformed how businesses connect with consumers. Marketing strategy, once confined to print and broadcast media, now embraces a dynamic, interactive, and data-driven paradigm.

1.3 The Symbiotic Relationship with Business Objectives

Alignment with Organizational Goals: The essence of marketing strategy lies in its symbiotic relationship with overarching business objectives. For a strategy to be effective, it must not only enhance brand visibility but also contribute directly to revenue generation, market share expansion, or other key performance indicators set by the organization.

Measuring Impact and Adjusting Course: An effective marketing strategy is not static; it evolves in response to market dynamics. This requires robust measurement mechanisms and a commitment to continuous improvement. Key performance indicators (KPIs) serve as compass points, allowing organizations to assess the impact of their strategies and make data-driven adjustments as needed.

Marketing strategy frameworks guides organizations through the dynamic landscape of business. It’s a holistic approach that integrates seamlessly with broader business objectives, adapts to the evolving digital landscape, and maintains a delicate balance between short-term tactics and long-term vision.

As postgraduate students aspiring to navigate the complexities of marketing, comprehending the essence of marketing strategy provides a solid foundation for the subsequent explorations into market research, segmentation, targeting, and positioning strategies. In the following sections, we will unravel the intricacies of these foundational elements, shedding light on their significance in crafting successful marketing strategy frameworks .

2. Market Research: The Foundations of Strategic Decision-Making

2.1 The Role of Market Research

Unveiling Insights for Informed Decisions – Market research stands as the bedrock of strategic decision-making, offering a systematic approach to gathering, analyzing, and interpreting information about a market, its dynamics, and its participants. At its core, market research seeks to unveil insights that empower businesses to make informed and data-driven decisions.

Types of Market Research: Quantitative Research: Involves the collection and analysis of numerical data. Surveys, questionnaires, and statistical techniques quantify market trends, preferences, and behaviors. This provides a numerical foundation for decision-making. Qualitative Research: Focuses on understanding the underlying motivations, attitudes, and perceptions of individuals. Techniques such as interviews, focus groups, and observational studies delve into the nuances that quantitative data may not capture.

Market Analysis Frameworks: SWOT Analysis: Examining Strengths, Weaknesses, Opportunities, and Threats provides a comprehensive view of both internal and external factors that can influence strategic decisions. PESTLE Analysis: Evaluating Political, Economic, Social, Technological, Legal, and Environmental factors helps businesses anticipate changes in the broader environment.

2.2 Consumer Behaviour Analysis

Navigating the Psychology of Purchasing Decisions – Understanding consumer behavior is a cornerstone of effective market research. It involves delving into the psychological, social, and economic factors that influence individuals’ buying decisions. Key components include:

Motivation: What drives consumers to make a purchase? Uncovering the underlying motivations helps businesses tailor their marketing messages and offerings.

Perception: How do consumers perceive a brand or product? Perception shapes purchasing decisions, and market research helps identify and influence these perceptions.

Attitude and Beliefs: Consumer attitudes and beliefs impact brand loyalty. Through in-depth analysis, businesses can identify and leverage these factors to build stronger connections with their target audience.

2.3 Incorporating Behavioral Economics in Strategy Formulation

Nudging Consumer Behavior – The field of behavioral economics introduces the concept of nudging – subtle interventions that influence decision-making. By understanding cognitive biases, businesses can strategically design marketing interventions that guide consumers towards desired actions.

Anchoring: The first piece of information encountered often influences subsequent decisions. Pricing strategies, for example, can leverage anchoring to shape perceived value.

Loss Aversion: Consumers tend to weigh potential losses more heavily than gains. Crafting marketing messages that highlight the potential loss of not choosing a product or service can be a persuasive tactic.

Market research serves as the compass that guides strategic decision-making. It unveils the intricacies of markets, consumer behaviors, and competitive landscapes, providing businesses with the insights needed to navigate complex terrain. As postgraduate students, mastering the art of market research equips us with the foundational skills required for effective strategic planning. In the following sections, we will explore the strategies of segmentation, targeting, and positioning, examining how market research forms the basis for these crucial components of a comprehensive marketing strategy.

Segmentation involves dividing a heterogeneous market into smaller, more homogeneous groups based on specific characteristics. This allows businesses to tailor their marketing strategies to the unique needs and preferences of each segment. Key aspects include:

Demographic Segmentation: Dividing the market based on demographics such as age, gender, income, education, and family size. This provides a foundational understanding of consumer profiles.

Psychographic Segmentation: Considering lifestyle, values, attitudes, and interests helps create segments with shared psychographic traits, enabling more targeted messaging.

Behavioral Segmentation: Analyzing purchasing behavior, brand loyalty, product usage, and other behavioral factors aids in grouping consumers with similar buying patterns.

Benefits of Segmentation: Targeted Marketing: By understanding the distinct needs of each segment, businesses can create marketing campaigns that resonate specifically with those groups.

Resource Efficiency: Resources are allocated more efficiently when marketing efforts are directed towards specific segments rather than a broad, undifferentiated market.

3.2 Targeting

Precision in Audience Selection – Targeting involves selecting specific segments to focus marketing efforts on. It’s about identifying the most lucrative and receptive audience for a product or service. Key targeting strategies include:

Undifferentiated Targeting: Appealing to the entire market with a single strategy. This approach is suitable when the product has broad appeal and little variation in consumer preferences.

Differentiated Targeting: Tailoring marketing strategies for different segments. This allows businesses to capture a larger market share by addressing diverse needs.

Concentrated Targeting: Concentrating efforts on a single, well-defined segment. This strategy is beneficial for niche markets where a specialized product can meet unique needs.

3.3 Positioning

Crafting a Distinct Brand Image: Positioning is about creating a distinctive and appealing image for a product or brand in the minds of consumers. It involves shaping perceptions to highlight unique selling propositions. Key elements of positioning include:

Value Proposition: Clearly communicating the value a product or service brings to consumers. This goes beyond features to emphasize the benefits and solutions it provides.

Brand Differentiation: Identifying and promoting aspects that set the brand apart from competitors. Whether it’s quality, innovation, or customer service, differentiation builds a competitive edge.

Perceptual Mapping: Visualizing how consumers perceive brands relative to competitors helps in fine-tuning positioning strategies.

Consistency Across Touchpoints: Consistency is crucial in positioning. Whether through advertising, customer service, or product experience, the brand’s positioning should remain coherent. This builds trust and reinforces the desired image in consumers’ minds.

The Segmentation, Targeting, Positioning (STP) framework is a cornerstone of effective marketing strategy. It transforms market research insights into actionable plans, allowing businesses to connect with specific audience segments in meaningful ways. As postgraduate students delving into the nuances of marketing strategy, understanding the intricacies of STP provides a roadmap for crafting compelling and targeted campaigns. In the subsequent sections, we will explore the dynamics of digital marketing in the 21st century, elucidating how STP strategies adapt to the ever-evolving landscape of online consumer engagement.

4. Digital Marketing in the 21st Century

4.1 The Digital Transformation and Marketing Strategy Frameworks

Shifting paradigms in consumer engagement. The 21st century has witnessed a profound transformation in how businesses connect with consumers, largely driven by the rise of digital platforms. Digital marketing encompasses a spectrum of online channels, tools, and strategies that redefine the way brands communicate, engage, and build relationships with their audience. Key aspects include:

Omni-channel Presence: Consumers seamlessly move between various online platforms. Successful digital marketing requires a cohesive presence across channels such as social media, search engines, email, and websites.

Personalization: Leveraging data and analytics, digital marketing allows for highly personalized interactions. Tailoring content, recommendations, and offers based on individual preferences enhances user experience and engagement.

4.2 Content Marketing and SEO Integration

Content marketing is at the heart of digital strategies, focusing on creating and distributing valuable, relevant, and consistent content to attract and retain a clearly defined audience. This involves:

Storytelling: Crafting narratives that resonate with the target audience builds emotional connections and enhances brand loyalty.

Multimedia Content: Embracing diverse content formats such as videos, infographics, and podcasts caters to varied consumer preferences.

The Art and Science of SEO Optimization: Search Engine Optimization (SEO) is instrumental in ensuring that digital content is discoverable by search engines, thereby reaching a wider audience. Key elements of SEO integration include:

Keyword Research: Identifying and incorporating relevant keywords enhances visibility in search engine results.

Quality Link Building: Building a network of high-quality backlinks improves domain authority and search rankings.

User Experience Optimization: Ensuring websites are mobile-friendly, have fast load times, and provide a seamless user experience contributes to higher search rankings.

Digital marketing in the 21st century is characterized by a dynamic interplay of technology, data, and consumer expectations. As postgraduate students exploring the nuances of marketing strategy, understanding the intricacies of digital marketing provides a lens into the evolving landscape of consumer engagement. In the upcoming sections, we will delve into the realm of social media strategies, exploring how businesses can harness the power of social platforms to amplify their brand presence, foster engagement, and navigate the intricacies of the digital age.

5. Social Media Strategies for Brand Amplification

5.1 Harnessing the Power of Social Media

Building Communities and Fostering Engagement – In the digital era, social media has emerged as a dynamic and influential platform for brand communication. Social media strategies go beyond mere presence; they aim to build communities, foster engagement, and amplify brand messages. Key components include:

Content Variety: Diversifying content types – from visually appealing images and videos to informative infographics and thought-provoking articles – ensures a well-rounded and engaging social media presence.

Consistent Brand Voice: Establishing a consistent brand voice across social platforms contributes to brand recognition and fosters a sense of authenticity.

Two-Way Communication: Social media is inherently interactive. Encouraging dialogue, responding to comments, and actively engaging with the audience build a sense of community and trust.

5.2 Influencer Marketing

Navigating the Landscape of Influencer Partnerships. Influencer marketing has become a powerful strategy within social media, leveraging individuals with significant online followings to promote products or services. Key considerations in influencer marketing include:

Relevance and Authenticity: Aligning with influencers whose values and audience align with the brand ensures authenticity and credibility.

Micro-Influencers: Partnering with influencers with smaller but highly engaged audiences often leads to more meaningful connections and conversions.

Transparency and Disclosure: Maintaining transparency about influencer partnerships builds trust with the audience and adheres to ethical standards.

5.3 Crisis Management in the Social Media Era

Proactive Measures and Damage Control – While social media offers immense opportunities for brand amplification, it also poses challenges in the form of rapid information dissemination and potential crises. Effective crisis management on social media involves:

Proactive Monitoring: Constantly monitoring social media channels enables swift identification of potential issues before they escalate.

Transparent Communication: In the event of a crisis, transparent and timely communication is crucial. Addressing concerns openly and honestly helps rebuild trust.

Learning from Incidents: Post-crisis analysis provides valuable insights for refining social media strategies and preventing similar incidents in the future.

Social media strategies are integral to brand amplification in the digital age. As postgraduate students navigating the complexities of marketing strategy, understanding the dynamics of social media allows us to harness the power of online communities, influencers, and effective crisis management. In the following sections, we will explore the critical aspects of measuring success in marketing, diving into the realm of Key Performance Indicators (KPIs) and data-driven decision-making.

Aligning Metrics with Business Goals – Effectively measuring the success of marketing strategies requires the definition and tracking of Key Performance Indicators (KPIs) that align with overarching business objectives. KPIs serve as quantifiable benchmarks, providing insights into the performance of various marketing initiatives. Key considerations include:

Business Objectives: Identifying the primary goals of marketing strategy frameworks – whether it’s increasing brand awareness, driving sales, or enhancing customer loyalty – informs the selection of relevant KPIs.

SMART Criteria: Ensuring that KPIs are Specific, Measurable, Achievable, Relevant, and Time-bound ensures clarity and effectiveness in evaluation.

6.2 Data-Driven Decision Making

Incorporating Analytics into the Decision-Making Process – The advent of advanced analytics tools has revolutionized the way businesses approach decision-making. In the context of marketing, leveraging data analytics is pivotal for making informed and strategic choices. Key components of data-driven decision-making include:

Data Collection and Analysis: Establishing robust data collection mechanisms and employing analytical tools help transform raw data into actionable insights.

Attribution Modeling: Understanding how various touchpoints contribute to conversions allows for more accurate attribution of success to specific marketing channels.

A/B Testing: Conducting controlled experiments with A/B testing provides empirical evidence on the effectiveness of different strategies, enabling refinement for optimal results.

6.3 Adapting Strategies Based on Performance Insights

Continuous Improvement Through Iterative Analysis – Measuring success is not a one-time task; it’s an ongoing process of evaluation, adjustment, and optimization. Constantly adapting strategies based on performance insights ensures agility and relevance. Key aspects include:

Regular Reporting: Establishing a regular reporting cadence allows for timely assessment of KPIs and performance against benchmarks.

Benchmarking Against Competitors: Comparing performance metrics with industry benchmarks and competitors provides context and identifies areas for improvement.

Iterative Testing: Embracing a culture of continuous improvement involves iteratively testing new ideas, analyzing results, and incorporating learnings into future strategies.

Measuring success in marketing is not merely about tracking numbers; it’s about deriving meaningful insights that inform strategic decisions. As postgraduate students immersed in the world of marketing strategy, understanding the intricacies of KPIs and data-driven decision-making empowers us to navigate the complexities of the digital landscape. In the final sections, we will delve into contemporary challenges faced by marketing professionals and explore emerging trends that shape the future of marketing strategy Frameworks.

7. Challenges and Future Trends in Marketing Strategy Frameworks

7.1 Contemporary Challenges

Adapting to Dynamic Market Conditions – The fast-paced nature of the business landscape introduces a set of challenges that marketers must navigate. Staying ahead in the face of these challenges requires strategic foresight and adaptability. Key contemporary challenges include:

Rapid Technological Advancements: The pace of technological evolution introduces both opportunities and challenges. Marketers must continually assess and adopt emerging technologies to stay relevant.

Consumer Empowerment: Empowered by information and choices, modern consumers demand personalized experiences, ethical practices, and transparency. Meeting these expectations poses a challenge for brands.

Navigating Ethical Considerations in Marketing – As consumers become more socially conscious, ethical considerations in marketing become increasingly important. Balancing business goals with ethical practices involves:

Authenticity and Transparency: Authenticity in messaging and transparent communication build trust. Ethical marketing practices involve truthfulness in advertising and fulfillment of promises.

Social Responsibility: Embracing corporate social responsibility (CSR) initiatives and sustainable practices aligns with consumer values and contributes to a positive brand image.

7.2 Future Trends in Marketing Strategy Frameworks

Artificial Intelligence and Automation – The integration of artificial intelligence (AI) and automation into marketing strategies is a defining trend. Key applications include:

Data Analysis and Personalization: AI enables advanced data analysis, allowing for more granular customer segmentation and personalized marketing strategies.

Chatbots and Virtual Assistants: Automated customer service through chatbots and virtual assistants enhances efficiency and provides instant support to consumers.

Sustainability as a Strategic Imperative As environmental concerns take center stage, sustainability becomes a key consideration in marketing strategy. Trends in sustainable marketing include:

Green Marketing: Emphasizing environmentally friendly practices in products, packaging, and operations to appeal to eco-conscious consumers.

Ethical Sourcing: Communicating responsible sourcing of materials and fair labor practices in marketing messages.

In the dynamic landscape of marketing strategy, challenges and trends are intertwined. As postgraduate students aspiring to master the art of marketing, understanding and addressing contemporary challenges while staying attuned to future trends is imperative. Navigating technological shifts, meeting ethical expectations, and embracing sustainability are integral aspects of crafting strategies that resonate with both current and future consumers.

The journey from defining marketing strategy and understanding market research to navigating digital marketing, social media strategies, measuring success, and addressing challenges and trends provides a comprehensive framework for postgraduate students seeking to excel in the field of marketing strategy. As we look towards the future, the ability to adapt, innovate, and integrate ethical and sustainable practices will be crucial in shaping successful marketing strategies in an ever-evolving business landscape.

By understanding these key aspects, postgraduate students and aspiring marketers can equip themselves with the knowledge and skills necessary to navigate the complexities of the ever-changing marketing strategy frameworks. If you enjoyed reading this post, I would be very grateful if you could help spread this knowledge by emailing this post to a friend, or sharing it on Twitter or Facebook. Thank you.

Women Entrepreneurs Dissertation – The aim of this dissertation is to explore the push-pull theory regarding women’s entrepreneurship in India. Similar to women in other parts of the world, Indian women are progressively broadening their horizons and gaining recognition in the professional domain. They are no longer confined to traditional domestic roles.

Various factors, including social, economic, political, psychological, and familial influences, are motivating women to initiate their own businesses and enter the entrepreneurial sphere. The motivation for women to engage in entrepreneurship is driven by a combination of push and pull factors. Some women are prompted by negative aspects such as the lack of suitable employment opportunities and dissatisfaction with existing working conditions. Conversely, others are drawn into entrepreneurship by their passion and creativity.

This research seeks to analyze these factors and assess the extent of their impact. It includes a comprehensive review of existing literature that explores the diverse factors influencing women in entrepreneurship, accompanied by relevant facts and figures. The push-pull theory is examined, supported by detailed charts and graphical evidence.

The central research question posed is “How does the push-pull theory influence women entrepreneurs in India?” The paper adopts an inductive research approach, exploring the emerging phenomenon of women entrepreneurship. The qualitative data collection and analysis method involve semi-structured interviews with women entrepreneurs in India. The results of the interviews are analyzed, followed by a comprehensive discussion on various aspects related to women entrepreneurship in India.

Dissertation Objectives

Investigate the social, economic, political, psychological, and family factors that have contributed to the transformation of women’s roles in India

Conduct a comprehensive analysis of both push and pull factors influencing women’s decisions to become entrepreneurs in India

Assess the impact of women’s entrepreneurship on economic development in India

Investigate the role of education in empowering women to pursue entrepreneurial ambitions

Women Entrepreneurs India Dissertation

Dissertation Contents – Women Entrepreneurs in India

2 – Literature Review Women’s role in business and entrepreneurship Facts and Figures about Women Entrepreneurs in India Push and Pull Theory

3 – Research Methodology The research question: How does push and pull theory influence women entrepreneurs in India? Research Philosophy – Interpretivism Research Approach – Inductive Research Method – Qualitative Research Methodology – Phenomenology Typology of Phenomenological Methodologies Insider Research Time Horizon and Sampling – Cross-sectional Research Ethics Data Collection and Data Analysis Limitations Conclusion

4 – Findings and Analysis Introduction Analysis Women in Entrepreneurship Reasons for being in business Duration in business Number of employees Level of education and entrepreneurship Level of education of the women interviewed The “man” factor in entrepreneurship Country factor in entrepreneurship Level of satisfaction from business Exclusion of point of interest Discussion Push-Pull Factors

Did you find any useful knowledge relating to Women Entrepreneurs in India in this post? What are the key facts that grabbed your attention? Let us know in the comments. Thank you.

Innovations in Marketing Strategy – As a marketing graduate, I have been asked on a handful occasions on how best to outline innovations in marketing strategy. In today’s hyper-competitive business landscape, an effective marketing strategy is the key to unlocking success and sustaining growth. As graduate students of marketing, we understand the significance of formulating a well-thought-out marketing strategy that not only attracts customers but also builds long-term brand equity. In this comprehensive guide, we will delve into the intricacies of marketing strategy, exploring its fundamental concepts, elements, and how to craft a winning strategy that aligns with your business goals.

Before diving into the depths of crafting a marketing strategy, it is essential to grasp the foundational concepts that underpin innovations in marketing strategy.

Market Segmentation – Market segmentation is the process of dividing a broad target market into smaller, more manageable segments based on common characteristics. Graduate students of marketing must understand the importance of segmentation in tailoring their marketing efforts to the specific needs and preferences of different customer groups. Market segmentation and targeting are not static concepts but evolving strategies that adapt to changing consumer behaviors and technological advancements.

Market segmentation, a fundamental concept in marketing, involves dividing a diverse market into smaller, distinct segments based on shared characteristics or behaviors. This approach recognizes that not all consumers are alike and allows organizations to tailor their marketing efforts more effectively. Graduate students should explore various segmentation criteria, including demographic, geographic, psychographic, and behavioral factors, each providing unique insights into consumer behavior.

Once segments are identified, targeting comes into play. Targeting involves selecting one or more specific segments as the focus of marketing efforts. This strategic decision is essential for resource allocation and message customization. By understanding the characteristics and needs of the chosen segments, organizations can create personalized marketing campaigns, increasing the likelihood of resonating with their audience and building stronger brand-customer relationships.

In today’s digital age, market segmentation and targeting have evolved with the availability of big data and advanced analytics. These techniques remain the cornerstones of successful marketing strategies, enabling businesses to adapt and thrive in an ever-changing marketplace.

Target Audience – Identifying a target audience is a critical step in marketing strategy development. By defining your ideal customer persona, you can tailor your marketing efforts to resonate with their unique needs, behaviors, and preferences.

Identifying the right target audience is a pivotal aspect of marketing strategy. It involves a comprehensive understanding of customer demographics, behaviors, and preferences. By honing in on a specific audience, organizations can allocate resources more efficiently, tailor their messaging to resonate with the intended recipients, and ultimately drive higher conversion rates.

Targeting enables businesses to build meaningful connections with their ideal customers, fostering brand loyalty and advocacy. In today’s data-rich environment, graduate students must grasp the significance of defining and reaching the right target audience, as it forms the foundation of effective marketing campaigns.

SWOT Analysis: A Crucial Starting Point

One of the first tasks in crafting a marketing strategy is conducting a SWOT analysis. SWOT stands for Strengths, Weaknesses, Opportunities, and Threats. This analysis helps graduate students identify internal and external factors that can influence the success of their marketing strategy.

Strengths and Weaknesses – Evaluate your organization’s internal factors, such as your resources, capabilities, and market positioning. Identify your strengths, which you can leverage, and your weaknesses, which require improvement.

Opportunities and Threats – Examine external factors, including market trends, competition, and economic conditions. Identifying opportunities allows you to exploit market trends, while recognizing threats enables proactive mitigation strategies.

Crafting Your Unique Value Proposition

A compelling value proposition is the heart of any successful marketing strategy. It defines what sets your product or service apart from competitors and resonates with your target audience.

Unique Selling Proposition (USP) – Your USP should convey why your offering is superior or different from alternatives in the market. It should address the specific needs and pain points of your target audience. The Unique Selling Proposition (USP) is a vital element in marketing strategy. It encapsulates the distinctive qualities or benefits that set a product or service apart from competitors.

A well-defined USP resonates with consumers by addressing their specific needs or pain points. Graduate students should understand that a compelling USP not only attracts attention but also builds brand identity and customer loyalty. Effective USPs communicate value and create a memorable brand perception, contributing to the success of marketing campaigns in a crowded marketplace. Crafting a unique, resonant USP is a strategic imperative for businesses seeking a competitive edge.

Clear Brand Identity -Building a strong brand identity is integral to your marketing strategy. Graduate students should ensure that their brand message, visual elements, and tone of voice are consistent and aligned with their value proposition.

A clear brand identity is fundamental in conveying a brand’s values, personality, and promises consistently across all touch points. It involves defining elements such as the brand’s logo, color scheme, typography, and tone of voice. This identity acts as a visual and emotional anchor, allowing consumers to recognize and connect with the brand effortlessly. Graduate students should recognize that a well-defined brand identity builds trust, fosters brand loyalty, and sets the stage for effective, cohesive marketing strategies.

Developing Marketing Objectives and Goals

Effective marketing strategies are goal-driven. Establishing clear objectives and goals is crucial for tracking progress and measuring the success of your strategy.

Specific, Measurable, Achievable, Relevant, and Time-Bound (SMART) Goals: Graduate students must craft SMART goals that are specific, quantifiable, attainable, relevant to the strategy, and bound by a timeframe. These goals serve as benchmarks for success.

Key Performance Indicators (KPIs) – Identify the KPIs that will be used to measure the performance of your marketing efforts. These may include metrics like website traffic, conversion rates, and customer retention.

Selecting Marketing Channels – Selecting the right marketing channels is essential for reaching your target audience effectively. Graduate students must consider the following:

Digital Marketing – In today’s digital age, online channels such as social media, email marketing, search engine optimization (SEO), and pay-per-click (PPC) advertising play a pivotal role. Choose the channels that align with your audience’s online behavior.

Digital marketing encompasses a wide array of strategies and channels, from social media and content marketing to SEO and email campaigns. It leverages the vast online landscape to reach and engage target audiences effectively. In today’s digital age, graduate students must grasp the dynamism of digital marketing, where consumer behaviors, algorithms, and platforms continuously evolve.

By understanding this multifaceted field, marketers can harness the power of digital marketing to expand their reach, enhance brand visibility, and drive conversions in an increasingly interconnected world.

Traditional Marketing – Depending on your target audience and industry, traditional marketing channels like print advertising, direct mail, and television can still be effective. Evaluate their relevance to your strategy.

Traditional marketing comprises strategies that have been fundamental to the field for decades, including print advertising, direct mail, television, radio, and outdoor advertising. These methods, though considered “traditional,” remain relevant in certain contexts and industries.

For graduate students, it’s essential to recognize that traditional marketing channels offer unique advantages, such as broad reach and tangibility. Understanding when and how to integrate traditional marketing into a comprehensive strategy is crucial, ensuring a well-rounded approach that capitalizes on both digital and traditional channels to achieve marketing objectives effectively.

Implementation and Execution

Once your marketing strategy is in place, the execution phase is where the rubber meets the road. Graduate students should:

Create a Marketing Calendar – Develop a detailed timeline that outlines when and how each marketing activity will be executed. This helps ensure consistency and accountability.

Allocate Resources – Ensure that you have the necessary resources, including budget, personnel, and technology, to implement your strategy effectively.

Continuous Monitoring and Adaptation

Marketing strategy is not static; it requires continuous monitoring and adaptation to remain effective. Graduate students should:

Regularly Analyze Data – Use data analytics to track the performance of your marketing efforts. Adjust your strategy based on the insights gained from customer behavior and performance metrics.

Stay Informed – Keep abreast of industry trends, market shifts, and emerging technologies that may impact your strategy. Adapt and innovate to stay ahead of the competition.

Innovations in Marketing Strategy Project

Conclusion Innovations in Marketing Strategy

In the ever-evolving world of marketing, graduate students must master the art of crafting effective marketing strategies that drive business success. By understanding the basics, conducting a SWOT analysis, developing a compelling value proposition, setting clear objectives, selecting the right marketing channels, and executing with precision, you can create a strategy that resonates with your target audience and achieves your business goals. Remember that successful marketing is an ongoing journey, requiring continuous monitoring, adaptation, and innovation to stay ahead in the competitive landscape.

References

Kotler, P., & Armstrong, G. (2017). Principles of Marketing. Pearson.

Payne, A., & Frow, P. (2014). Developing a wider perspective on corporate reputation management. Journal of Brand Management, 21(9), 693-699.

Pulizzi, J., & Barrett, N. (2015). Content Inc.: How Entrepreneurs Use Content to Build Massive Audiences and Create Radically Successful Businesses. McGraw-Hill Education.

Hsu, C. L., & Tsou, K. H. (2019). How social media influencers build a brand? Strategies and challenges. Sustainability, 11(7), 1868.

Kaplan, A. M., & Haenlein, M. (2010). Users of the world, unite! The challenges and opportunities of Social Media. Business Horizons, 53(1), 59-68.

Lee, M., & Youn, S. (2009). Electronic word of mouth (eWOM): How eWOM platforms influence consumer product judgment. International Journal of Advertising, 28(3), 473-499.

Smith, A. N., & Noble, S. M. (2014). The impact of social media usage on consumer purchasing behavior. Journal of Retailing, 90(3), 363-376.

Kim, A. J., & Ko, E. (2012). Do social media marketing activities enhance customer equity? An empirical study of luxury fashion brand. Journal of Business Research, 65(10), 1480-1486.

Escalas, J. E. (2007). Narrative processing: Building consumer connections to brands. Psychology & Marketing, 24(8), 713-741.

Did you find any useful knowledge relating to innovations in marketing strategy in this post? What are the key facts that grabbed your attention? Let us know in the comments. Thank you.

Multiple Regression SPSS GSSS Dataset Project – Multiple regression is a statistical analysis technique used to examine the relationship between a dependent variable (the outcome or response variable) and two or more independent variables (predictors or explanatory variables). In other words, it allows you to predict the value of the dependent variable based on the values of the independent variables.

SPSS (Statistical Package for the Social Sciences) is a widely used software for statistical analysis in various fields, including social sciences, business, and other research domains. It provides tools to perform a wide range of statistical analyses, including multiple regression.

The GSS (General Social Survey) dataset is a well-known dataset in the social sciences, particularly in sociology. The GSS is a survey conducted in the United States that collects data on a wide range of topics, such as demographics, attitudes, and behaviors. Researchers use the GSS dataset to analyze trends and relationships in society.

Multiple Regression Background

A “Multiple Regression SPSS GSSS Dataset” refers to the application of multiple regression analysis using the GSS dataset within the SPSS software. This could involve analyzing the relationship between one or more dependent variables (e.g., income, happiness, political affiliation) and several independent variables (e.g., age, education, gender) using the GSS dataset and the statistical capabilities of SPSS.

Research question:

The effect of age, number of children, respondent’s income and weekly working hours on the overall family income.

Research hypothesis:

H0: age, number of children, respondent’s income and weekly working hours has no effect on the family’s income.

H1: age, number of children, respondent’s income and weekly working hours has an effect on the family’s income.

Research design:

The research design adopted in this study is referred to as causal relationship approach with the aim of analyzing the effect of age, number of children, respondent’s income and weekly working hours on the overall family income. According to (Cooper & Schindler, 2014), the main concern in causal relationship approach is with how one variable(s) affects or is responsible for changes in another variable(s).

Dependent variable:

The dependent variable(Y) used was the family income. The income was measured in constant dollars showing how much income the whole family generates.

Independent variables:

(X1) the first independent variable is the number of children in each family

(X2) respondent’s income measured in constant dollars is the second variable

(X3) weekly working hours is the last independent variable which is measured by the number of hours the respondent works in a week.

Control variables:

Control variables are the held constant in order to assess the relationship between other variables (Allison, P. D., 1990). This research has included two control variable which are the sex of the respondents and their ages. These variables are added because in a typical society the sex affects the income of the worker and the higher the age the greater the experience hence increased income. By setting the two variable as control we excluded their effect on the model.

Descriptive Statistics

Mean

Std. Deviation

N

FAMILY INCOME IN CONSTANT DOLLARS

56199.86

48030.037

32

NUMBER OF HOURS USUALLY WORK A WEEK

39.69

12.880

32

NUMBER OF CHILDREN

2.59

1.720

32

RESPONDENT INCOME IN CONSTANT DOLLARS

31446.56

30660.828

32

AGE OF RESPONDENT

47.88

12.289

32

RESPONDENTS SEX

1.69

.471

32

Model Summary

Model

R

R Square

Adjusted R Square

Std. Error of the Estimate

Change Statistics

R Square Change

F Change

df1

df2

Sig. F Change

1

.744a

.554

.468

35040.004

.554

6.449

5

26

.001

a. Predictors: (Constant), RESPONDENTS SEX, AGE OF RESPONDENT, NUMBER OF HOURS USUALLY WORK A WEEK, NUMBER OF CHILDREN, RESPONDENT INCOME IN CONSTANT DOLLARS

Coefficients

Model

Unstandardized Coefficients

Standardized Coefficients

T

Sig.

B

Std. Error

Beta

1

(Constant)

15653.406

51982.735

.301

.766

AGE OF RESPONDENT

1684.865

667.954

.431

2.522

.018

NUMBER OF CHILDREN

-11618.887

4835.608

-.416

-2.403

.024

RESPONDENT INCOME IN CONSTANT DOLLARS

.851

.330

.543

2.579

.016

NUMBER OF HOURS USUALLY WORK A WEEK

-20.512

767.766

-.006

-.027

.979

RESPONDENTS SEX

-21296.312

16254.030

-.209

-1.310

.202

a. Dependent Variable: FAMILY INCOME IN CONSTANT DOLLARS

Results:

A multiple regression test was carried out to test if number of children in a family, respondent’s income and number of hours worked weekly affect the overall family income. From the SPSS output the independent variable affect the dependent variable. The model summary table show that r=0.74, r2=0.554 thus, there is a positive correlation between the predictor and the response variables.

Additionally, 55.4% of the variation in the family income (M= 56199.86, SD= 48030.037, N= 32) is explained by variations in the dependent variables. From the f value F= 6.449, p=0.001, the f change tests for overall significance of the independent variable in the model and p value< 0.05 we therefore reject the null hypothesis (Anderson et al., 2000) and conclude that the independent variable are statistically significance hence they affect the family income.

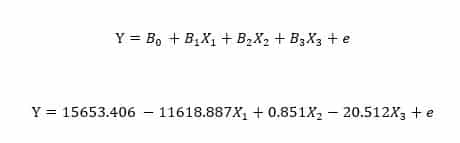

The coefficient tables gives rise to the models regression equation:

Where:

Y= family income in constant dollars

X1= number of children in the family

X2= respondent’s income in constant dollars

X3= number of hours worked weekly.

e= noise

X1 (M=2.59,SD=1.720,N=32) is statistically significant at t=-2.403,p=0.024 because the p value is less than 0.05, the effect size is at -11618.887 such that an increase in children number in the family ceteris paribus leads to a decrease in family income by 11618.887dollars.

X2(M=31446.56, SD=30660.828, N=32) is also statistically significant at t=2.579, p= 0.016 being less than 0.05 we reject the null hypothesis and conclude that the respondent’s income affects the family income. The effect size is such that an increase in the respondent’s income by one dollar ceteris paribus leads to an increase in the family income by 0.851.

X3(M=39.69, SD=12.880,N=32) is not statistically significant, t=-0.027, p=0.979,the p-value being greater than 0.05 we accept the null hypothesis that respondent’s number of weekly working hours does not affect the family’s income.

In conclusion we establish from the statistics that, other than sex and age of the respondent the family’s income is affected by the number of children in the family and the respondent’s income holding other factors constant.

References

Allison, P. D. (1990). Change Scores as Dependent Variables in Regression Analysis. Sociological Methodology, 20, 93.

Cadotte, M. W., & Davies, T. J. (2018). Randomizations, Null Distributions, and Hypothesis Testing. Princeton University Press.

Cooper, D. R., & Schindler, P. S. (2014). Business Research Methods. New York, NY: McGraw Hill Education.

David, Anderson R., Burnham, K. P., & Thompson, W. L. (2000). Null hypothesis testing: Problems, prevalence, and an alternative. Journal of Wildlife Management, 64(4), 912-923

Did you find any useful knowledge relating to multiple regression SPSS GSSS datasets in this post? What are the key facts that grabbed your attention? Let us know in the comments. Thank you.